Q3 2025 Review

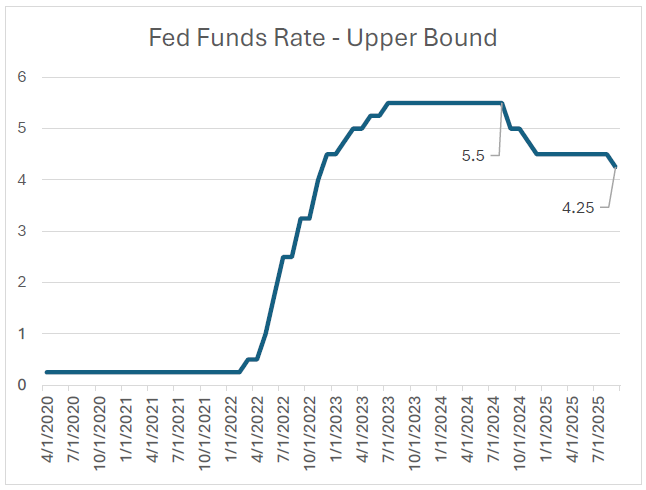

The third quarter of 2025 was marked by continued volatility in interest rates, persistent inflation concerns, and growing debate over the trajectory of Federal Reserve policy. From June 30 through September 30, longer-term Treasury yields remained elevated as markets wrestled with resilient economic data and uncertainty surrounding trade and fiscal policy. While inflation has moderated from its peak, progress toward the Fed’s 2% target has been uneven, keeping rate expectations fluid and the yield curve sensitive to incoming data. We are 1 year into the easing cycle by the Federal Reserve, and the Upper Bound on the Fed Funds Rate is now at 4.25% (Below).

Source: Bloomberg

The Case for Cutting Rates

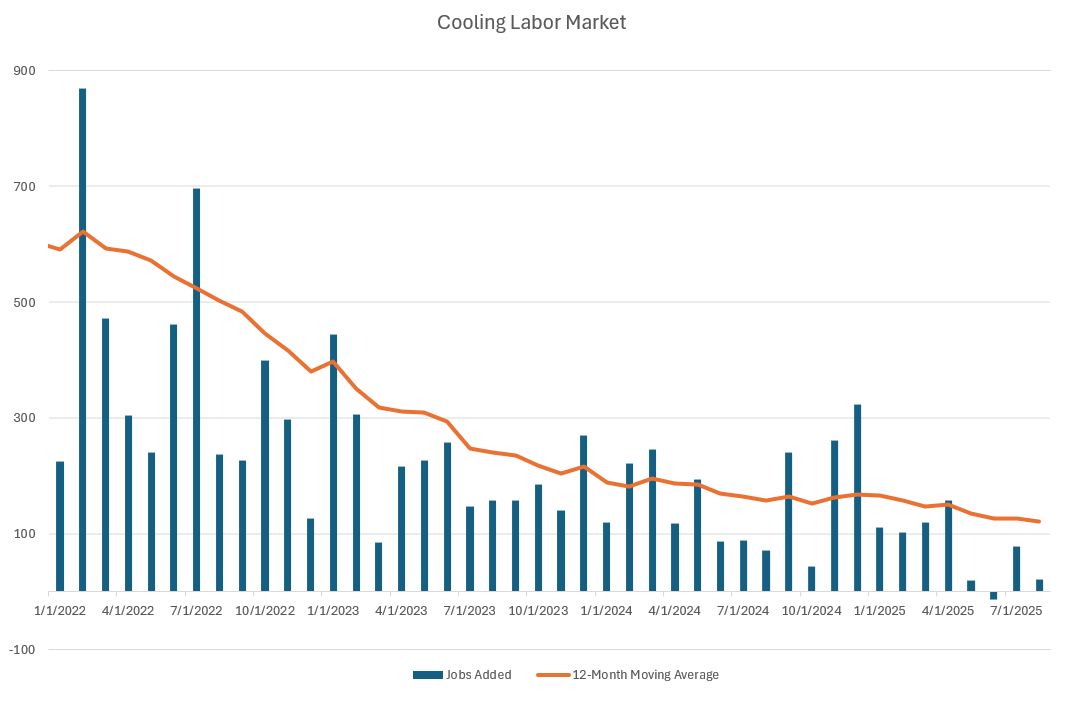

The labor market (seen below) has cooled steadily over the past few years, which is not surprising given the extraordinary strength seen during the COVID recovery. This moderation has helped rebalance the Federal Reserve’s dual mandate. Even with inflation remaining elevated, the Fed has continued to cut rates to come to the aid of the jobs market. In our view, the emphasis has shifted—stabilizing the labor market and preventing further increases in unemployment (now 4.3%) appears to have taken priority over maintaining restrictive policy to push inflation fully back to 2%.

Source: Bloomberg

The Housing Affordability Crisis

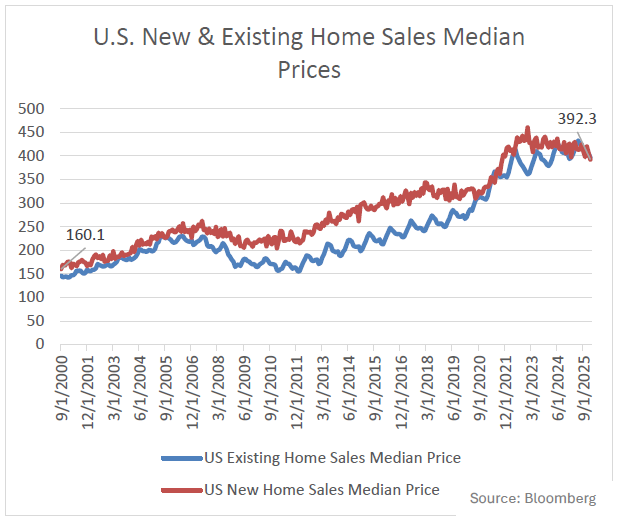

The median home price for a new home in the United States has risen from $160,000 to just under $400,000 since the year 2000. This is an increase of 145% in 25 years. The Fed tightened rates from 2022-2024. This has helped prices come down slightly from the peak in early 2023 of $460,000 for the median price of a new home. This is encouraging for new buyers as builders have increased incentives to sell more homes. As seen below, this is one of the only times that new homes have been cheaper than existing home prices. Builders have been quicker to cut prices as existing homeowners are more reluctant to let go of equity built up over the past few years.

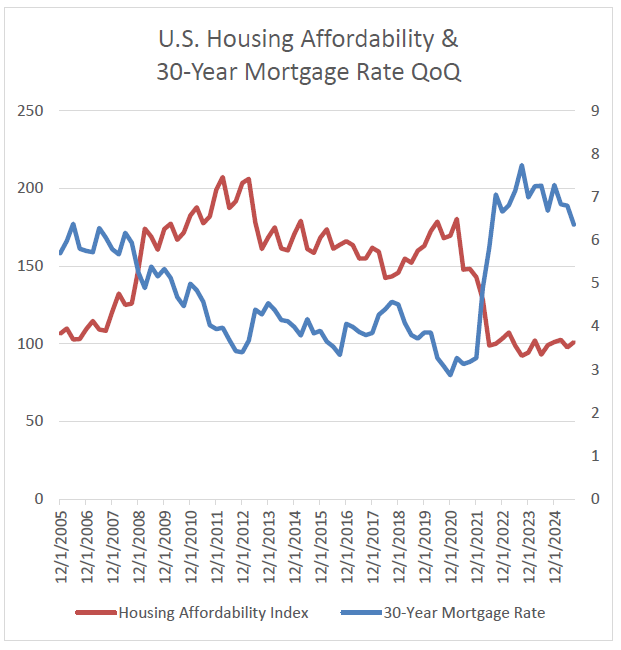

For home buyers, nominal wage growth has not kept up with increasing home prices. According to the BLS, nominal wages for middle-income workers have barely doubled from $30,108/year to $63,180/year from 2000 to 2025. So, while home prices have gone up 145%, nominal middle-class income has increased by only 110%. As seen below, housing affordability has never been worse.

Source: Bloomberg

Conclusion

While the overall economy has remained strong, we continue to watch consumer spending, which is the primary driver of the American economy. Lower-income households appear the most strained but have remained resilient. Munis continue to offer a haven if this should change.