Q1 2026 Review

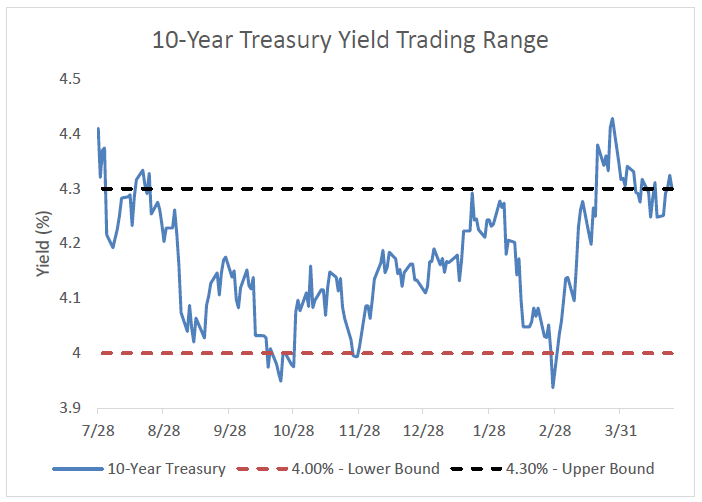

The 10-Year Treasury yield (shown below) moved below 4.30% in July 2025 and has mostly traded within a relatively tight 4.00%–4.30% range for the past nine months. Over the past year, yields have approached the 4.00% level multiple times, but each instance has been met with resistance. Most recently, we dipped below 4.00% on 2/27 - the day before the U.S. and Israel launched coordinated military strikes against Iran. Rates have risen since then as expectations of rate cuts have dwindled and the conflict continues.

Source: Bloomberg

Muni Rates Over the Past Month

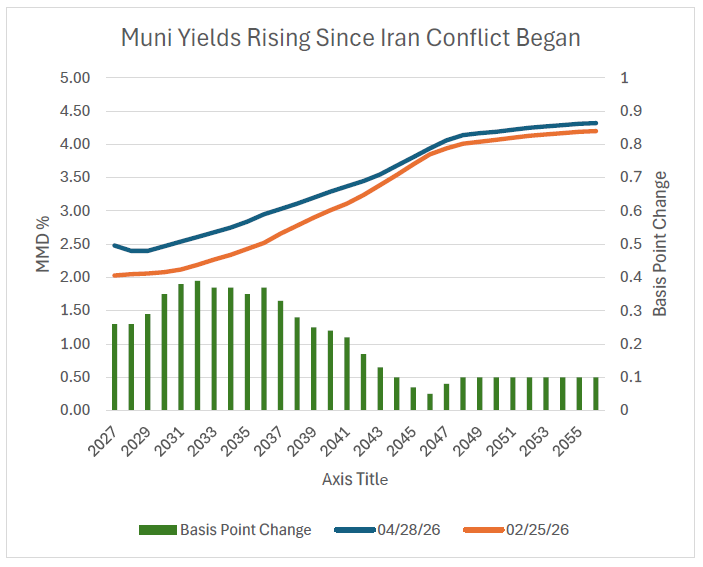

The Iran conflict has pushed municipal yields higher as well (below). Particularly on the short end of the curve, rates have jumped nearly 40 basis points since late February. That move reflects a market that is rapidly unwinding its rate cut assumptions. The speed of this repricing underscores how quickly fixed income markets can adjust when assumptions around policy and inflation shift. While a swift resolution to the conflict could reverse some of this quickly, we believe it is wise to structure portions of our client’s portfolios around a higher-for-longer rate environment until there is more clarity.

Source: Bloomberg

Oil Prices, the U.S. Economy, and Long-Term Interest Rates

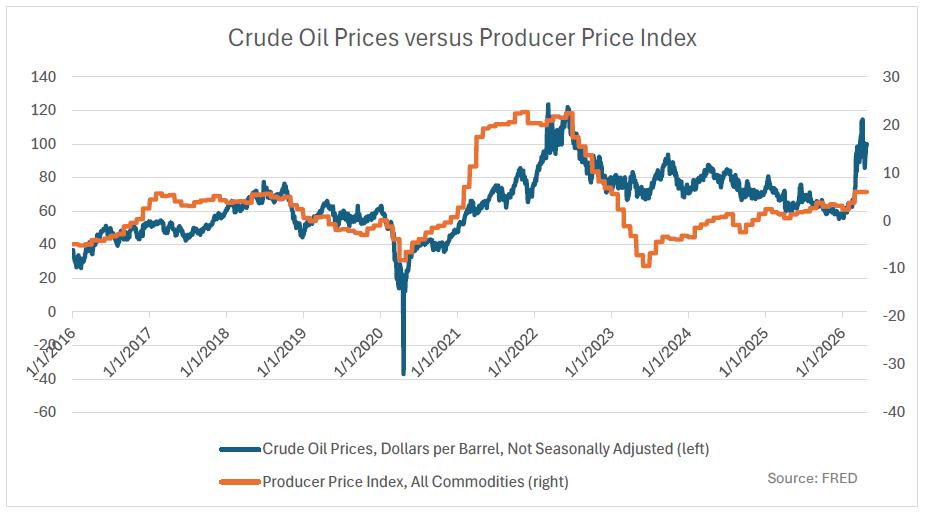

Oil prices play a significant role in shaping the U.S. economy and long-term interest rates. Because energy is a core input across transportation, manufacturing, and consumer activity, a spike in oil prices often creates ripple effects through inflation and economic growth.

Spikes In Oil Prices Correlate with Higher Inflation

The most immediate impact of rising oil prices is higher inflation. Increased costs for gasoline, heating, and transportation feed directly into measures such as CPI and PCE. Businesses facing higher input costs frequently pass those increases on to consumers, reinforcing inflationary pressures. Historically, this has led to a moderate positive correlation between oil prices and inflation, often in the 0.4 to 0.6 range.

Higher Oil Prices Act Like a Tax Increase

At the same time, higher oil prices tend to slow economic growth. As households spend more on energy, discretionary spending declines. Businesses may reduce investment or hiring due to rising costs. In this way, oil shocks often act as a tax on economic activity.

Long-term U.S. interest rates reflect the balance between these two forces. When inflation concerns dominate, long-term Treasury yields typically rise as investors demand greater compensation for future purchasing power risk. However, if higher oil prices significantly weaken growth, yields may fall as markets anticipate slower economic activity and potential Federal Reserve easing.

For investors, this highlights an important dynamic: oil-driven inflation can push yields higher in the short term, but growth deterioration can ultimately pull rates lower over time. As shown below, producer prices in the U.S. have climbed steadily while oil prices have remained elevated, pointing to the influence of energy costs on overall goods pricing.

Municipalities and Reducing Cybersecurity Risk

Nearly 30 years ago as public issuers proactively assessed, remediated and disclosed their Y2K readiness, actual disruptions were rare and the financial impact was minimal. Cybersecurity, however, presents a very different and ongoing challenge. Municipal issuers now face continuous threats to data integrity and operational resilience from attacks that can disrupt essential services and undermine investor confidence. Unlike Y2K—a one-time event that was largely contained through coordinated preparation—cyber threats evolve constantly and require sustained attention.

The Y2K experience offers useful lessons: advance planning, transparent disclosure, public awareness and stakeholder collaboration all reduced risk then and remain critical today. Public finance issuers are adopting similarly disciplined approaches to cybersecurity by implementing clear policies, governance structures and ethical frameworks, regularly testing defenses, and communicating risk to investors and the public.

Today the public sector is engaging in the following to improve cyber security:

Modernization of IT infrastructure-moving to cloud-based platforms

Employee training-avoiding phishing attacks

Strengthening incidence response frameworks-formal response plans

Cyber insurance-working with the private sector

Partnering with state and federal agencies, as well as private firms

These measures reflect a shift toward a more disciplined approach to cybersecurity and will hopefully help reduce the stress associated with unwanted cyber-attacks on our public systems.

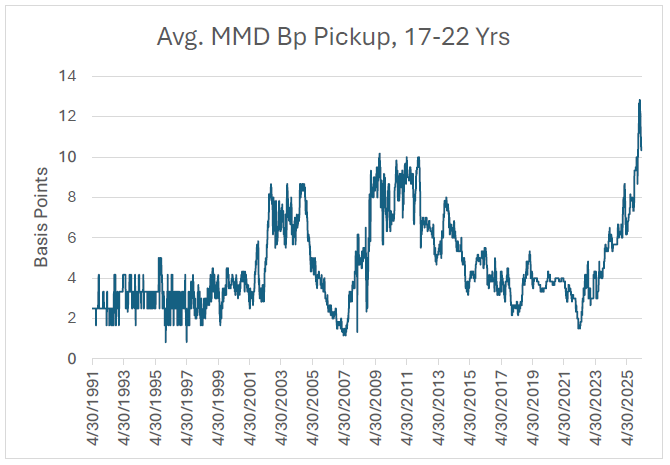

Muni Yield Curve is Steep

The 17–22-year range of the municipal yield curve (roughly 2043-2048 maturities) is at its steepest level since our data began in 1991. Investors are currently earning about 12 basis points of additional yield for each extra year of maturity, creating an incentive to extend duration modestly. By moving slightly further out into the 20-22-year range, investors can lock in higher yields with minimal additional risk. This has been a great time for investors to take advantage of the curve and lock in these yields with good call protection

Source: MMD, TFS

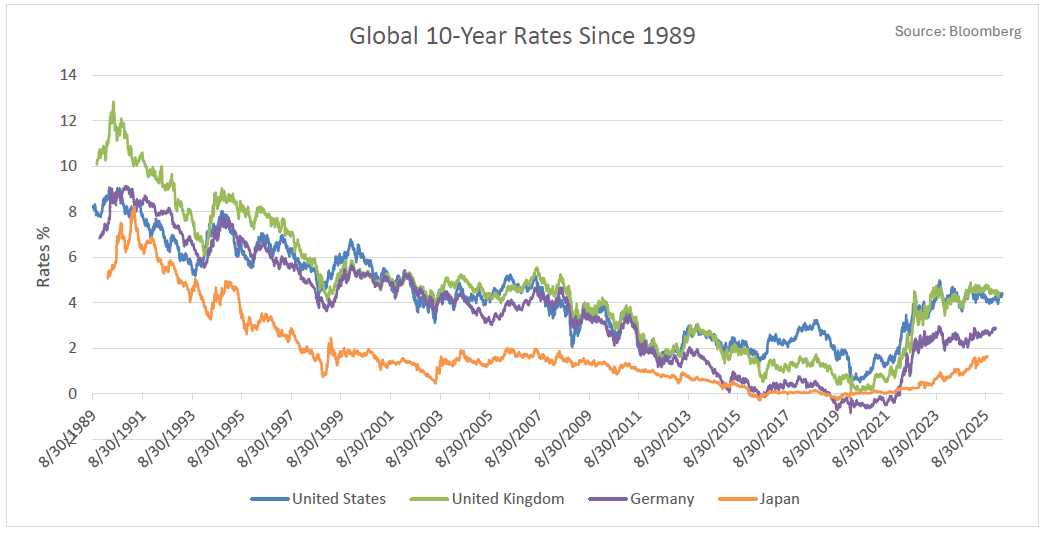

Global Rates Remain Elevated

As shown below, from approximately 2010-2021 we saw an economic backdrop of lower rates. This meant governments, corporations, and municipalities were able to finance debt at historically low levels. It was an era of ‘easy money’ and led to strong economic activity and encouraged borrowing, investment, and consumption. As global rates began to rise in 2022, there have been ripple effects everywhere. For governments, the cost of issuing new debt has risen and now face higher interest expense as older debt rolls off. Corporations face this same issue, so weaker companies face increased margin pressure. Consumers have seen mortgage, credit card, and auto loan rates increase sharply along with rising prices. Everyone has had to adjust to tighter financial conditions.

For Muni Bond investors, rates are now extremely attractive. After years of lower rates, we are able to lock up higher yields, protect client income streams, and build Muni Bond portfolios with Tax-Equivalent yields in the 7-8% range. We continue to build portfolios to weather weakness in the economy but are finding Munis incredibly attractive in this economic backdrop.

Conclusion

As markets continue to navigate shifting rate expectations and geopolitical developments, we expect volatility to remain a defining feature in the near term. However, the current backdrop of higher yields allows investors to be more selective, emphasizing income, quality, and disciplined positioning across municipal portfolios.